Towing a Boat or Trailer in Texas: Is It Covered by Your Auto Insurance?

Head out to Canyon Lake or down to the Guadalupe on any summer weekend and you’ll see them lined up bumper to bumper: pickups towing bass boats, ski boats, utility trailers, and the occasional camper. It’s one of the most common questions we hear at our New Braunfels office: “If my truck is insured, is the boat or trailer behind it covered too?”

The honest answer is partly — and the part most people get wrong is the part that costs them thousands. Let’s clear it up in plain English.

The one distinction almost everyone misses

Here’s the rule that trips people up:

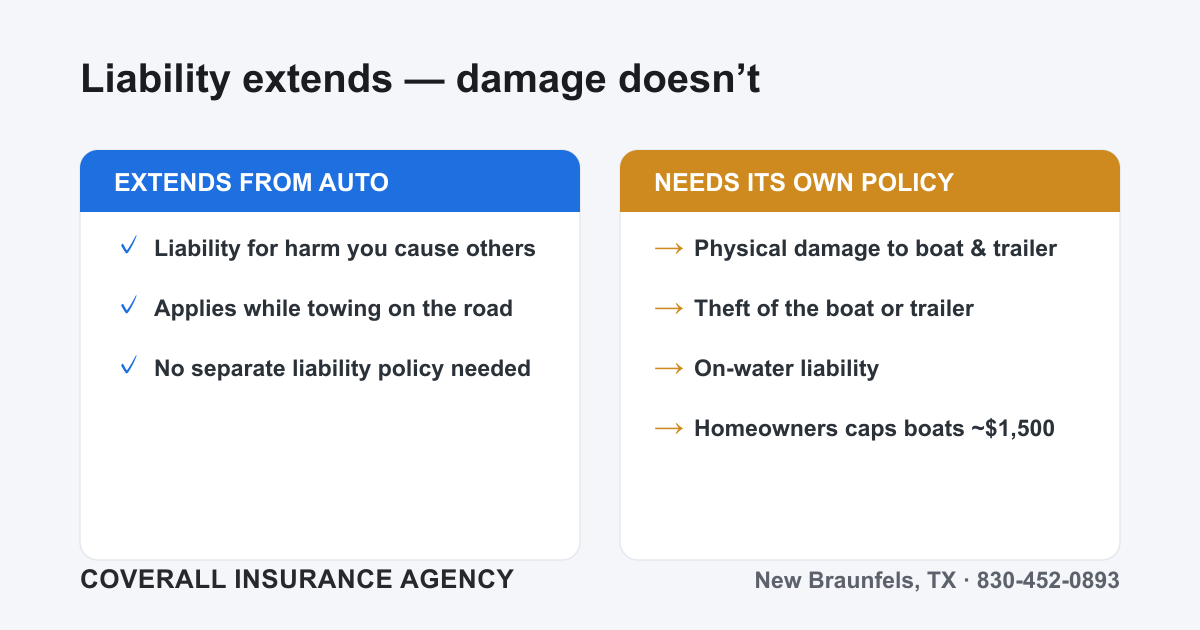

Your auto policy’s liability coverage generally extends to a trailer or boat you’re towing. Your auto policy’s physical damage coverage (collision and comprehensive) generally does not.

In practice, that means:

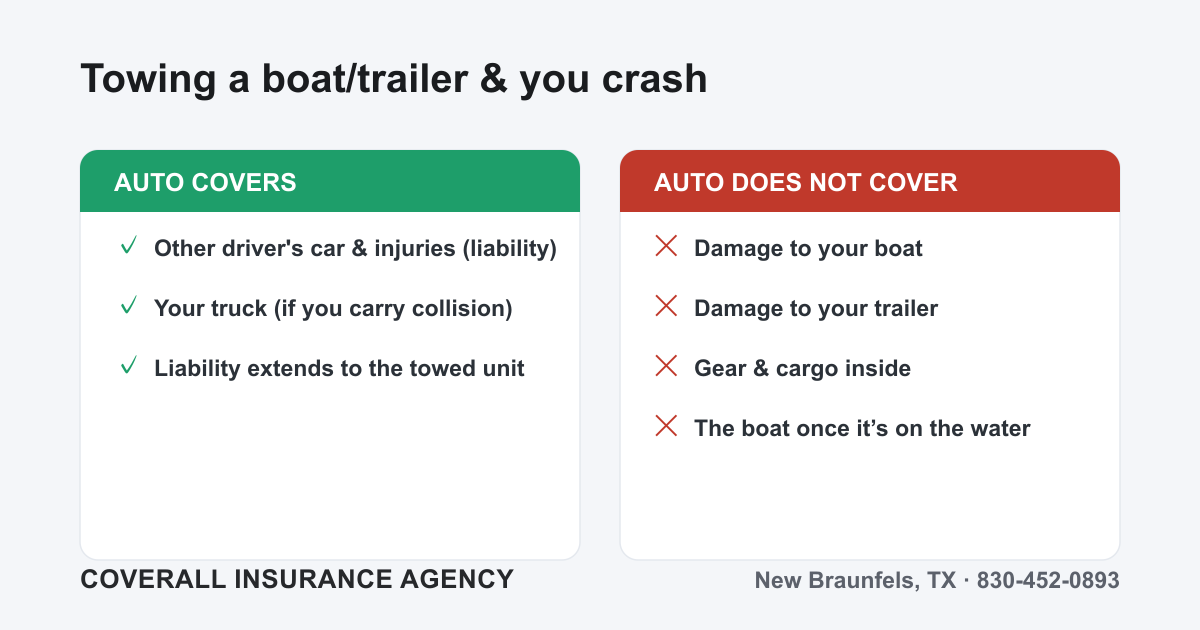

- If you cause a wreck while towing, your auto liability coverage typically pays for the injuries and property damage you cause to other people — even though those damages may have been caused or worsened by the trailer or boat swinging behind you.

- Your own boat or trailer, if it’s damaged, stolen, or destroyed, is not covered by your auto policy in most cases. Auto liability protects the other guy. It does nothing for your stuff.

So “my truck is insured” is true and useful — but it only covers half of what’s actually at risk on that drive to the lake. Learn more about how those coverages work on our auto insurance page.

Utility and cargo trailers: liability extends, damage doesn’t

Pulling a flatbed, an enclosed cargo trailer, or a utility trailer to haul a mower, ATV, or furniture? The same split applies.

- Liability extends. If your trailer fishtails into another car or the load shifts and causes an accident, your auto liability generally responds for the harm done to others.

- Physical damage usually does NOT extend. If your own trailer is damaged in that same crash, dented by hail, or stolen out of a parking lot, your auto policy typically won’t pay to repair or replace it.

- The cargo isn’t covered either. The tools, equipment, or furniture inside that trailer are generally not covered by your auto policy. Depending on what it is, your homeowners insurance might offer limited help — but often it won’t, especially for business property.

To actually protect the trailer itself and what’s on it, you typically need a separate trailer policy or a trailer added (scheduled) onto another policy.

Boats: auto won’t cover the watercraft — on the road OR the water

Boats add a second layer of confusion, because there are two environments where damage can happen: on the trailer behind your truck, and in the water.

- On the road: Auto liability extends to the boat-and-trailer rig you’re towing (damage you cause to others). But your auto policy will not pay for damage to the boat itself if you jackknife on Highway 46 or someone rear-ends your rig.

- On the water: Your auto policy stops at the boat ramp. The moment that hull floats, auto insurance is completely out of the picture — no liability if you hit another boat, no coverage if you hit a submerged stump, nothing.

What about homeowners? A standard homeowners policy gives you only very limited boat coverage — typically a small dollar cap (often around $1,000–$1,500) and usually only for small, low-horsepower boats. A real ski boat, bass boat, or wake boat is almost always excluded or wildly underinsured under a homeowners policy.

That’s why a dedicated boat / watercraft policy exists. It covers the boat on the road and on the water — physical damage, theft, and on-water liability — and a good one usually extends coverage to the trailer too. We can set that up through our recreational vehicle insurance options.

Weight and type limits — read the fine print

Even the liability that does extend to your trailer isn’t unlimited. Auto policies frequently carve out:

- Trailers above a certain weight or size (heavy equipment trailers, gooseneck/fifth-wheel rigs)

- Trailers used for business rather than personal use

- Certain boat sizes or horsepower beyond what the policy contemplates

If your rig is bigger than what your policy assumes, even the liability extension can come into question. When in doubt, ask — don’t guess.

The scenario: what’s covered vs. not when you’re towing and crash

Picture this. You’re towing your $40,000 bass boat down FM 306 toward Canyon Lake. You look down for two seconds, drift, and clip a sedan. The sedan is totaled, the driver goes to the ER, your boat is cracked along the hull, and your trailer axle is bent.

You’re at fault. Here’s how the claims shake out:

- The other driver’s car and injuries → Paid by your auto liability. ✅

- Your truck → Paid by your auto collision coverage (if you carry it). ✅

- Your boat (cracked hull) → NOT covered by auto. Only a boat policy pays this. ❌ → ✅ only if you have boat insurance

- Your trailer (bent axle) → NOT covered by auto in most cases. Covered by a boat or trailer policy that includes the trailer. ❌ → ✅ only with the right policy

- The fishing gear and electronics in the boat → Generally not covered by auto; sometimes partially by a boat policy or homeowners. ❌

Now flip it — you’re NOT at fault. Say that sedan ran a stop sign and hit your rig:

- The at-fault driver’s liability insurance should pay for your truck, boat, and trailer damage and any injuries.

- But if they’re uninsured or underinsured (common in Texas), you’re back to relying on your own coverages — your uninsured/underinsured motorist coverage for the truck, and your boat policy for the boat and trailer. Without a boat policy, you could be stuck chasing a driver who has no money to collect.

The lesson: whether you’re at fault or not, the only thing that reliably protects your boat and trailer is a policy that actually covers your boat and trailer.

Bottom line

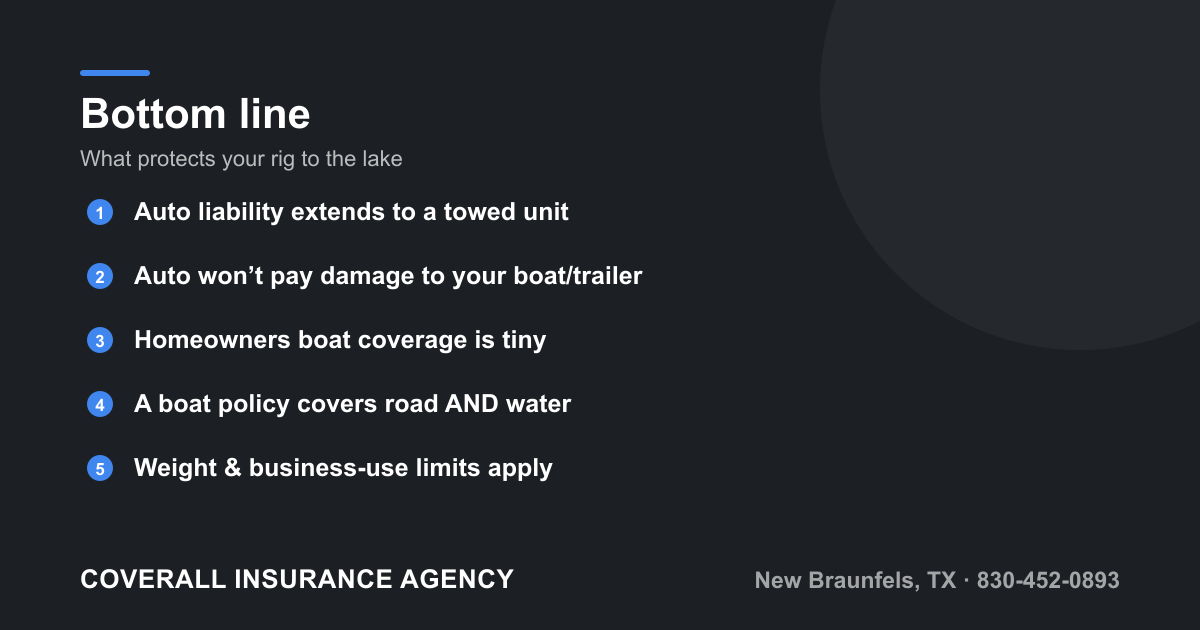

- Auto liability extends to a towed trailer or boat — it covers the damage you cause to others. ✅

- Auto collision/comprehensive generally does NOT extend to your boat or trailer — your own watercraft and trailer are on their own. ❌

- Homeowners gives only tiny, capped boat coverage — fine for a canoe, useless for a real boat.

- A boat/watercraft policy is what actually protects the boat (and usually the trailer) — on the road and on the water.

- Weight, size, and business-use limits can shrink even the liability that does extend, so confirm your specific rig.

Out here in the Hill Country, towing to the lake is just part of the lifestyle. Make sure the boat and trailer you spent real money on aren’t riding to the ramp with zero protection.

Want to know exactly what your truck, boat, and trailer are — and aren’t — covered for? Get a free, no-pressure quote on our contact page or call our New Braunfels team at 830-452-0893. We’ll make sure every link in your rig is covered before your next trip to Canyon Lake.